Comprehensive Financial Plan for HNWI

Investment Advisory Report

by Ivan Jaben Pang , Lim Chang shun Brian, Lee Sheng Jue Luke, Nurmuhammad Amzari

Client Profile

Client Profile

Client Profile

Fig 1.1

According to the family background of our client’s family, they have 3 family members in the household. Our client, who is currently 48 years old, has a spouse (Angie) and a child (Elaine), who are 45 and 16 years old respectively. There is only one income earner, David (the father), who earns $60,000 per month. Angie, his spouse, currently does not have a job but can get a job paying $9,000 per month if necessary. David has investments in Singapore Equities and REITS that are valued at $400,000. David and Angie have a combined CPF balance of $450,000 and savings of $400,000. The family owns a property that is worth $4,500,000 where there is $1,500,000 remaining on mortgage. House contents are worth $400,000. The family also owns a BMW that is worth $310,000 where there is a $120,000 outstanding car loan. Their total net worth is $4,827,000. (refer to Fig 1.1 for breakdown).

Fig 1.1

According to the family background of our client’s family, they have 3 family members in the household. Our client, who is currently 48 years old, has a spouse (Angie) and a child (Elaine), who are 45 and 16 years old respectively. There is only one income earner, David (the father), who earns $60,000 per month. Angie, his spouse, currently does not have a job but can get a job paying $9,000 per month if necessary. David has investments in Singapore Equities and REITS that are valued at $400,000. David and Angie have a combined CPF balance of $450,000 and savings of $400,000. The family owns a property that is worth $4,500,000 where there is $1,500,000 remaining on mortgage. House contents are worth $400,000. The family also owns a BMW that is worth $310,000 where there is a $120,000 outstanding car loan. Their total net worth is $4,827,000. (refer to Fig 1.1 for breakdown).

Fig 1.2

Our client’s family has $8,000 in monthly savings and has a monthly expense of $49,500. (refer to Fig 1.2 in Appendices for breakdown)

David has life insurance and critical illness coverage of $2,000,000 and $500,000, respectively. The family is also covered with health insurance which is paid for by David’s employer. The family has no wills, investment plans, savings plans, or any estate and legacy planning.

Elaine will go through tertiary education and aims to pursue university studies and postgraduate studies. The client needs to ensure that he has enough funds for his child’s education.

Our client aims to retire at 65 years old with a monthly income of at least $20,000. They also plan to purchase an apartment to invest in and pass it over to their daughter, Elaine, when she eventually gets married. Finally, our client wishes to sell his BMW to purchase a Tesla Model Y ($280,000) for his spouse and an Audi e-Tron ($400,000) for himself.

Our client considers having a will, as they currently do not have one. They also wish to ensure that their daughter is financially taken care of when they pass on. This includes having an inheritance of $3,000,000 for her.

Recommendation for 5-Year Portfolio Plan

My High-Net-Worth Clients, David and Angie Wee, are a married couple aged 48 and 45, with a daughter named Elaine aged 16. They have a total monthly income of S$60K and aim to purchase an investment property for their child and pass down their inheritance to ensure their daughter lives comfortably when they pass on. Currently, they are in the Consolidation Phase of their Life Cycle and have a medium risk appetite. Hence, their portfolios should be diversified into 20% Cash, 30% Bonds and 50% Equity.

The World Economic Forum (WEF) in its Global Risk Report 2023, has identified the global cost of living crisis as the biggest risk over the next two years. Due to disruptions in food and energy supplies, as well as China's plans to reopen, energy prices have risen 46 percent since last year, contributing to higher global inflation. The International Monetary Fund predicts a drop in inflation, but the FED and Western Central Banks are worried about low unemployment leading to higher inflation for longer periods, causing the FED to push for a deeper-than-expected recession. The WEF has an optimistic outlook towards a recession, which could lower interest rates and reduce bank default risk. However, the WEF predicts a Polycrisis, a cluster of global risks caused by a shortage of natural resources leading to resource competition and control among countries, in the next 2 to 7 years.

We plan to protect our client's portfolio from the upcoming Polycrisis by avoiding Sustainable Development Growth (SDG) investments and including Environmental, Social and Governance (ESG) Investments as the World Economic Forum (WEF) has centralized their plans around ESGs. We are avoiding SDGs as one example of a similar past occurrence is the failure of the Millennium Development Goals in 2008.

Fig 1.2

Our client’s family has $8,000 in monthly savings and has a monthly expense of $49,500. (refer to Fig 1.2 in Appendices for breakdown)

David has life insurance and critical illness coverage of $2,000,000 and $500,000, respectively. The family is also covered with health insurance which is paid for by David’s employer. The family has no wills, investment plans, savings plans, or any estate and legacy planning.

Elaine will go through tertiary education and aims to pursue university studies and postgraduate studies. The client needs to ensure that he has enough funds for his child’s education.

Our client aims to retire at 65 years old with a monthly income of at least $20,000. They also plan to purchase an apartment to invest in and pass it over to their daughter, Elaine, when she eventually gets married. Finally, our client wishes to sell his BMW to purchase a Tesla Model Y ($280,000) for his spouse and an Audi e-Tron ($400,000) for himself.

Our client considers having a will, as they currently do not have one. They also wish to ensure that their daughter is financially taken care of when they pass on. This includes having an inheritance of $3,000,000 for her.

Our client’s family has $8,000 in monthly savings and has a monthly expense of $49,500. (refer to Fig 1.2 in Appendices for breakdown)

David has life insurance and critical illness coverage of $2,000,000 and $500,000, respectively. The family is also covered with health insurance which is paid for by David’s employer. The family has no wills, investment plans, savings plans, or any estate and legacy planning.

Elaine will go through tertiary education and aims to pursue university studies and postgraduate studies. The client needs to ensure that he has enough funds for his child’s education.

Our client aims to retire at 65 years old with a monthly income of at least $20,000. They also plan to purchase an apartment to invest in and pass it over to their daughter, Elaine, when she eventually gets married. Finally, our client wishes to sell his BMW to purchase a Tesla Model Y ($280,000) for his spouse and an Audi e-Tron ($400,000) for himself.

Our client considers having a will, as they currently do not have one. They also wish to ensure that their daughter is financially taken care of when they pass on. This includes having an inheritance of $3,000,000 for her.

Recommendation for 5-Year Portfolio Plan

My High-Net-Worth Clients, David and Angie Wee, are a married couple aged 48 and 45, with a daughter named Elaine aged 16. They have a total monthly income of S$60K and aim to purchase an investment property for their child and pass down their inheritance to ensure their daughter lives comfortably when they pass on. Currently, they are in the Consolidation Phase of their Life Cycle and have a medium risk appetite. Hence, their portfolios should be diversified into 20% Cash, 30% Bonds and 50% Equity.

The World Economic Forum (WEF) in its Global Risk Report 2023, has identified the global cost of living crisis as the biggest risk over the next two years. Due to disruptions in food and energy supplies, as well as China's plans to reopen, energy prices have risen 46 percent since last year, contributing to higher global inflation. The International Monetary Fund predicts a drop in inflation, but the FED and Western Central Banks are worried about low unemployment leading to higher inflation for longer periods, causing the FED to push for a deeper-than-expected recession. The WEF has an optimistic outlook towards a recession, which could lower interest rates and reduce bank default risk. However, the WEF predicts a Polycrisis, a cluster of global risks caused by a shortage of natural resources leading to resource competition and control among countries, in the next 2 to 7 years.

We plan to protect our client's portfolio from the upcoming Polycrisis by avoiding Sustainable Development Growth (SDG) investments and including Environmental, Social and Governance (ESG) Investments as the World Economic Forum (WEF) has centralized their plans around ESGs. We are avoiding SDGs as one example of a similar past occurrence is the failure of the Millennium Development Goals in 2008.

Fig 2.1

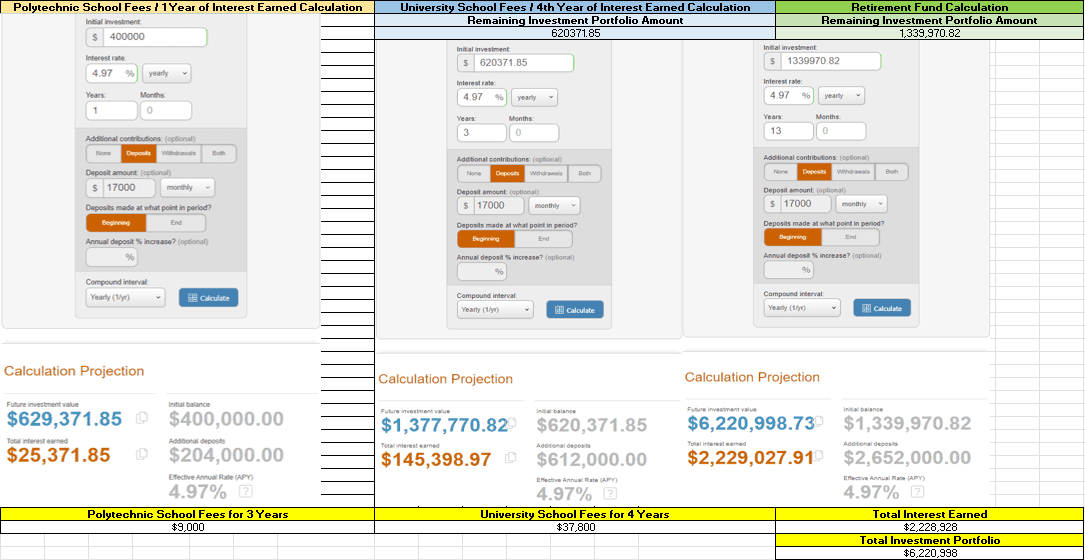

For our client’s Investment Portfolio, we would suggest our clients deposit $17,000 monthly into their initial $400,000 investment to be compounded. As we are heading into a “Low Growth, Low Investment & Low Cooperation Era” based on the WEF, I would allocate 20% of portfolio assets into Cash holdings as cash is one of the best hedges against recession. To achieve the highest rate of returns on Cash Holdings, we would open a UOB One Savings Account which offers 3.85% Interest Per Annum for our clients to store their cash holdings. While the other 30% of our client’s portfolio will be diversified into ESG Bonds, such as the Procter & Gamble Company TheDL-Notes 5.55% Coupon Bond that holds a Low-Risk Rating, reflecting P&G’s solid financial position and ESG initiatives. Finally, 25% of our client investment portfolio will be invested into dividend stocks such as the Intel Corporation NASDAQ: INTC Stock which has a dividend yield of 5.19%, while the last 25% will be invested into REITS such as Keppel Corporation Limited which provides a dividend yield of 4.96%. The expected annual rate of return of the Investment Portfolio is 4.97%. (Refer to Figure 2.1)

Elaine's Education Planning

Fig 2.1

For our client’s Investment Portfolio, we would suggest our clients deposit $17,000 monthly into their initial $400,000 investment to be compounded. As we are heading into a “Low Growth, Low Investment & Low Cooperation Era” based on the WEF, I would allocate 20% of portfolio assets into Cash holdings as cash is one of the best hedges against recession. To achieve the highest rate of returns on Cash Holdings, we would open a UOB One Savings Account which offers 3.85% Interest Per Annum for our clients to store their cash holdings. While the other 30% of our client’s portfolio will be diversified into ESG Bonds, such as the Procter & Gamble Company TheDL-Notes 5.55% Coupon Bond that holds a Low-Risk Rating, reflecting P&G’s solid financial position and ESG initiatives. Finally, 25% of our client investment portfolio will be invested into dividend stocks such as the Intel Corporation NASDAQ: INTC Stock which has a dividend yield of 5.19%, while the last 25% will be invested into REITS such as Keppel Corporation Limited which provides a dividend yield of 4.96%. The expected annual rate of return of the Investment Portfolio is 4.97%. (Refer to Figure 2.1)

For our client’s Investment Portfolio, we would suggest our clients deposit $17,000 monthly into their initial $400,000 investment to be compounded. As we are heading into a “Low Growth, Low Investment & Low Cooperation Era” based on the WEF, I would allocate 20% of portfolio assets into Cash holdings as cash is one of the best hedges against recession. To achieve the highest rate of returns on Cash Holdings, we would open a UOB One Savings Account which offers 3.85% Interest Per Annum for our clients to store their cash holdings. While the other 30% of our client’s portfolio will be diversified into ESG Bonds, such as the Procter & Gamble Company TheDL-Notes 5.55% Coupon Bond that holds a Low-Risk Rating, reflecting P&G’s solid financial position and ESG initiatives. Finally, 25% of our client investment portfolio will be invested into dividend stocks such as the Intel Corporation NASDAQ: INTC Stock which has a dividend yield of 5.19%, while the last 25% will be invested into REITS such as Keppel Corporation Limited which provides a dividend yield of 4.96%. The expected annual rate of return of the Investment Portfolio is 4.97%. (Refer to Figure 2.1)

Elaine's Education Planning

Fig 2.2

With the assumption that Elaine is an express student in secondary school who is completing her O-levels and polytechnic studies over a span of 4 years, Elaine would be entering her polytechnic school within one year's time and her university in four years. Hence, with our clients' calculated expected rate of return of 4.97% per year, there would be a total accumulated dividends/interest earned of $25,371.85 within a year. With a course fee of $9,000 over the span of 3 Years, our client’s total dividends/interest earned would definitely be enough to pay off their daughters' polytechnic fees. After deducting $9,000 from our client’s Total Investment Portfolio to pay for school fees, they would accumulate a total dividends/interest earnings of $145,398.97 over the next 3 years. As such, our client’s total dividends/interest earned would definitely be more than sufficient to pay off their daughter’s NTU Environmental Engineering School fees of $37,800 over the span of 4 academic years. (Refer to Figure 2.2)

Real Estate Planning

With the Landed Property Market soaring within the past two years, from a 13.3% Increase in 2021 to a 9.5% Increase in 2022, Landed Property prices are expected to ease this year. Hence, this would be a perfect time for our clients to exit the Landed Property Market to purchase two new investment homes. Assuming that our client’s current Upper Thomson home is bought under both of their names, their goal of purchasing an investment property for their child faces a major roadblock of having to pay an extra 17% ABSD Tax to purchase a second property. Our solution to this issue would be to either decouple the ownership of their current property or sell their current home to purchase two separate private properties under separate names. Due to our client’s outstanding $1.5m mortgage loan, the second option would be more viable. Hence, if our clients were to sell off their property at a valuation of $4.5m, paying off their mortgage would leave them with $3 million in cash.

Based on Singapore’s Master Plan, we will be leveraging Major Urban Transformations to drive our property asset investments. For our client’s own stay, we have chosen a two-bedroom unit at Reflections at Keppel Bay, priced at $1.65m. As part of the Great Southern Waterfront (GSW) Transformation Plan, the construction of 9000 new units near Reflections is soon to occur, driving Reflections owners to let go of their properties at extremely low prices. We can see evidence of this with similar 2-bedroom units transacted at a $2m range in May 2022. With new upcoming condo developments in GSW, new record-high prices will be set in the region. Additionally, with the Singapore Government bringing in more High Net Worth Individuals from abroad, the demand for luxury iconic condominiums will also drive up the prices of Reflections at Keppel Bay.

Fig 2.3

As for our client’s investment property, we have chosen a 1-bedroom unit at Watertown which is a mixed-development condominium located beside Punggol MRT, priced at $889,000. As part of the Punggol Digital District (PDD) Transformation Plan, Punggol would be known as a “Smart District” and the home of the Singapore Institute of Technology’s campus alongside JTC’s Business Park, housing important digital economy growth sectors like cybersecurity and technology, while also serving as a diverse and sustainable way of life for residences. On completion of the PDD Transformation, Watertown Condominium’s Valuation is expected to drastically soar alongside its current high rental yield of 3.5% due to its huge tenant pool. (Refer to Figure 2.3 for breakdown)

Retirement Planning

Based on our client’s daughter's University Education fees as previously mentioned in the 5 Year Investment Plan, $37,800 would be withdrawn and deducted from their total investment portfolio, leaving them with $1,339,970.82 in investments. If our clients were to take our suggestion and continue compounding their earnings while faithfully making their monthly investment portfolio deposits, they would have earned a total of $2,229,027.91 in dividends/interest alone. With our client’s total estimated Investment Portfolio valued at $6,220,998.73 at the age of 65 after 17 years of investing, our clients would definitely be able to retire with way more than $20,000 a month for an assumed period of over 20 years.

Legacy & Estate Planning

In preparation for Legacy and Estate Planning, our client aims to provide their daughter, Elaine, with an inheritance of $3,000,000. On top of David’s current life insurance coverage of $2,000,000, we recommend David take on a Term Life insurance, PRUActive Term that provides coverage of $1.65m upon his death at a premium of $2,354 a month. David will pay off his premium by 65 years old, before retirement age. This ensures that when the time comes, Elaine will be left with $3,650,000 in cash inheritance based solely on insurance coverage to ensure her financial well-being. Additionally, we also recommend our clients, David and Angie Wee, produce an Attested Written Will in case of the death of a loved one. Without a Will that clearly states how the inheritance is distributed to each individual, the Intestate Law, which indicates for you what each survivor gets, would automatically be applied upon the death of a spouse. Hence, if David were to pass away without a will, the intestate law would apply, where all assets owned under his name would be divided in half so that his wife and child would get equal portions of the inheritance.

Proposed Budgeting Action Plan

Fig 2.2

With the assumption that Elaine is an express student in secondary school who is completing her O-levels and polytechnic studies over a span of 4 years, Elaine would be entering her polytechnic school within one year's time and her university in four years. Hence, with our clients' calculated expected rate of return of 4.97% per year, there would be a total accumulated dividends/interest earned of $25,371.85 within a year. With a course fee of $9,000 over the span of 3 Years, our client’s total dividends/interest earned would definitely be enough to pay off their daughters' polytechnic fees. After deducting $9,000 from our client’s Total Investment Portfolio to pay for school fees, they would accumulate a total dividends/interest earnings of $145,398.97 over the next 3 years. As such, our client’s total dividends/interest earned would definitely be more than sufficient to pay off their daughter’s NTU Environmental Engineering School fees of $37,800 over the span of 4 academic years. (Refer to Figure 2.2)

With the assumption that Elaine is an express student in secondary school who is completing her O-levels and polytechnic studies over a span of 4 years, Elaine would be entering her polytechnic school within one year's time and her university in four years. Hence, with our clients' calculated expected rate of return of 4.97% per year, there would be a total accumulated dividends/interest earned of $25,371.85 within a year. With a course fee of $9,000 over the span of 3 Years, our client’s total dividends/interest earned would definitely be enough to pay off their daughters' polytechnic fees. After deducting $9,000 from our client’s Total Investment Portfolio to pay for school fees, they would accumulate a total dividends/interest earnings of $145,398.97 over the next 3 years. As such, our client’s total dividends/interest earned would definitely be more than sufficient to pay off their daughter’s NTU Environmental Engineering School fees of $37,800 over the span of 4 academic years. (Refer to Figure 2.2)

Real Estate Planning

With the Landed Property Market soaring within the past two years, from a 13.3% Increase in 2021 to a 9.5% Increase in 2022, Landed Property prices are expected to ease this year. Hence, this would be a perfect time for our clients to exit the Landed Property Market to purchase two new investment homes. Assuming that our client’s current Upper Thomson home is bought under both of their names, their goal of purchasing an investment property for their child faces a major roadblock of having to pay an extra 17% ABSD Tax to purchase a second property. Our solution to this issue would be to either decouple the ownership of their current property or sell their current home to purchase two separate private properties under separate names. Due to our client’s outstanding $1.5m mortgage loan, the second option would be more viable. Hence, if our clients were to sell off their property at a valuation of $4.5m, paying off their mortgage would leave them with $3 million in cash.

Based on Singapore’s Master Plan, we will be leveraging Major Urban Transformations to drive our property asset investments. For our client’s own stay, we have chosen a two-bedroom unit at Reflections at Keppel Bay, priced at $1.65m. As part of the Great Southern Waterfront (GSW) Transformation Plan, the construction of 9000 new units near Reflections is soon to occur, driving Reflections owners to let go of their properties at extremely low prices. We can see evidence of this with similar 2-bedroom units transacted at a $2m range in May 2022. With new upcoming condo developments in GSW, new record-high prices will be set in the region. Additionally, with the Singapore Government bringing in more High Net Worth Individuals from abroad, the demand for luxury iconic condominiums will also drive up the prices of Reflections at Keppel Bay.

With the Landed Property Market soaring within the past two years, from a 13.3% Increase in 2021 to a 9.5% Increase in 2022, Landed Property prices are expected to ease this year. Hence, this would be a perfect time for our clients to exit the Landed Property Market to purchase two new investment homes. Assuming that our client’s current Upper Thomson home is bought under both of their names, their goal of purchasing an investment property for their child faces a major roadblock of having to pay an extra 17% ABSD Tax to purchase a second property. Our solution to this issue would be to either decouple the ownership of their current property or sell their current home to purchase two separate private properties under separate names. Due to our client’s outstanding $1.5m mortgage loan, the second option would be more viable. Hence, if our clients were to sell off their property at a valuation of $4.5m, paying off their mortgage would leave them with $3 million in cash.

Based on Singapore’s Master Plan, we will be leveraging Major Urban Transformations to drive our property asset investments. For our client’s own stay, we have chosen a two-bedroom unit at Reflections at Keppel Bay, priced at $1.65m. As part of the Great Southern Waterfront (GSW) Transformation Plan, the construction of 9000 new units near Reflections is soon to occur, driving Reflections owners to let go of their properties at extremely low prices. We can see evidence of this with similar 2-bedroom units transacted at a $2m range in May 2022. With new upcoming condo developments in GSW, new record-high prices will be set in the region. Additionally, with the Singapore Government bringing in more High Net Worth Individuals from abroad, the demand for luxury iconic condominiums will also drive up the prices of Reflections at Keppel Bay.

However, we do not recommend the client to use his savings to purchase the cars as cars will depreciate in value. Furthermore, purchasing more cars is not a necessity. The savings could be better used to invest to fund the client’s retirement and child education which are of higher priority. The client could purchase the 2 cars after he has sufficient funds for his higher priorities.

Refinancing Car Loan

The client plans to sell his current car and purchase 2 cars, worth $680,000. The Open Market Value (OMV) for the 2 cars are as follows:

Tesla Model Y - $68,691;

Audi e-Tron - $64,068

Since both cars have an OMV of more than $20,000, the client can only take up a 60% loan. The client will need to pay the remaining 40% in cash, which is $272,000. If the client sells his BMW and pays off his outstanding car loan, he will have a total of $190,000 cash. This is not enough to cover the downpayment of the 2 cars. The client will end up using his savings. (refer to Fig 3.3 for breakdown).

Payoff Outstanding Credit Card Balance

The client has an outstanding credit card balance of $13,000 and only pays the minimum balance every month. The client should pay off his credit card balance in full to avoid the huge 22% interest rate per annum. If not paid in full, the outstanding balance will accumulate every month. This leads to the client paying a higher interest over time. The client should use his savings to pay off the initial $13,000 outstanding credit card balance. The balance for subsequent months would be paid in full.

Fig 3.3

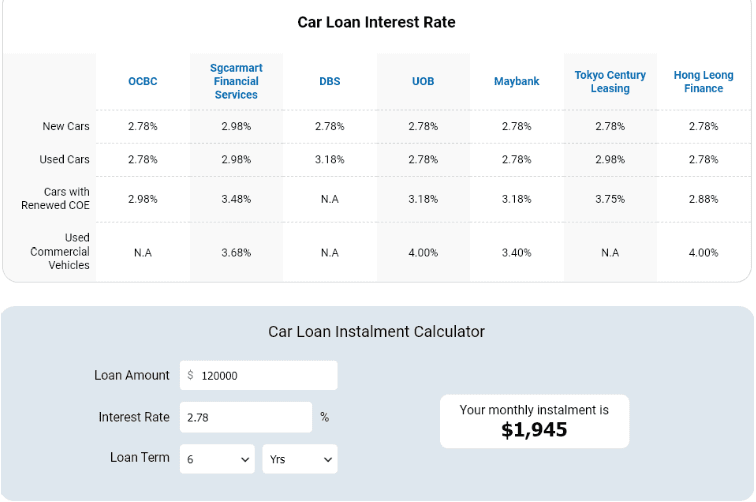

The client’s current monthly instalment for car loan is $8,000. The client is recommended to refinance his car loan to increase his cash flow. It is assumed that the client’s current car is approximately 1 year old. In accordance with MAS refinancing rules for motor vehicle loans, the client is able to refinance his car loan to a maximum tenure of 6 years. The client’s outstanding car loan is $120,000. When refinanced with DBS, the new monthly instalment for car loan is $1,945. This is a 75.7% decrease from the current monthly instalment. (refer to Fig 3.4/3.5).

Fig 2.3

As for our client’s investment property, we have chosen a 1-bedroom unit at Watertown which is a mixed-development condominium located beside Punggol MRT, priced at $889,000. As part of the Punggol Digital District (PDD) Transformation Plan, Punggol would be known as a “Smart District” and the home of the Singapore Institute of Technology’s campus alongside JTC’s Business Park, housing important digital economy growth sectors like cybersecurity and technology, while also serving as a diverse and sustainable way of life for residences. On completion of the PDD Transformation, Watertown Condominium’s Valuation is expected to drastically soar alongside its current high rental yield of 3.5% due to its huge tenant pool. (Refer to Figure 2.3 for breakdown)

As for our client’s investment property, we have chosen a 1-bedroom unit at Watertown which is a mixed-development condominium located beside Punggol MRT, priced at $889,000. As part of the Punggol Digital District (PDD) Transformation Plan, Punggol would be known as a “Smart District” and the home of the Singapore Institute of Technology’s campus alongside JTC’s Business Park, housing important digital economy growth sectors like cybersecurity and technology, while also serving as a diverse and sustainable way of life for residences. On completion of the PDD Transformation, Watertown Condominium’s Valuation is expected to drastically soar alongside its current high rental yield of 3.5% due to its huge tenant pool. (Refer to Figure 2.3 for breakdown)

Retirement Planning

Based on our client’s daughter's University Education fees as previously mentioned in the 5 Year Investment Plan, $37,800 would be withdrawn and deducted from their total investment portfolio, leaving them with $1,339,970.82 in investments. If our clients were to take our suggestion and continue compounding their earnings while faithfully making their monthly investment portfolio deposits, they would have earned a total of $2,229,027.91 in dividends/interest alone. With our client’s total estimated Investment Portfolio valued at $6,220,998.73 at the age of 65 after 17 years of investing, our clients would definitely be able to retire with way more than $20,000 a month for an assumed period of over 20 years.

Based on our client’s daughter's University Education fees as previously mentioned in the 5 Year Investment Plan, $37,800 would be withdrawn and deducted from their total investment portfolio, leaving them with $1,339,970.82 in investments. If our clients were to take our suggestion and continue compounding their earnings while faithfully making their monthly investment portfolio deposits, they would have earned a total of $2,229,027.91 in dividends/interest alone. With our client’s total estimated Investment Portfolio valued at $6,220,998.73 at the age of 65 after 17 years of investing, our clients would definitely be able to retire with way more than $20,000 a month for an assumed period of over 20 years.

Legacy & Estate Planning

In preparation for Legacy and Estate Planning, our client aims to provide their daughter, Elaine, with an inheritance of $3,000,000. On top of David’s current life insurance coverage of $2,000,000, we recommend David take on a Term Life insurance, PRUActive Term that provides coverage of $1.65m upon his death at a premium of $2,354 a month. David will pay off his premium by 65 years old, before retirement age. This ensures that when the time comes, Elaine will be left with $3,650,000 in cash inheritance based solely on insurance coverage to ensure her financial well-being. Additionally, we also recommend our clients, David and Angie Wee, produce an Attested Written Will in case of the death of a loved one. Without a Will that clearly states how the inheritance is distributed to each individual, the Intestate Law, which indicates for you what each survivor gets, would automatically be applied upon the death of a spouse. Hence, if David were to pass away without a will, the intestate law would apply, where all assets owned under his name would be divided in half so that his wife and child would get equal portions of the inheritance.

In preparation for Legacy and Estate Planning, our client aims to provide their daughter, Elaine, with an inheritance of $3,000,000. On top of David’s current life insurance coverage of $2,000,000, we recommend David take on a Term Life insurance, PRUActive Term that provides coverage of $1.65m upon his death at a premium of $2,354 a month. David will pay off his premium by 65 years old, before retirement age. This ensures that when the time comes, Elaine will be left with $3,650,000 in cash inheritance based solely on insurance coverage to ensure her financial well-being. Additionally, we also recommend our clients, David and Angie Wee, produce an Attested Written Will in case of the death of a loved one. Without a Will that clearly states how the inheritance is distributed to each individual, the Intestate Law, which indicates for you what each survivor gets, would automatically be applied upon the death of a spouse. Hence, if David were to pass away without a will, the intestate law would apply, where all assets owned under his name would be divided in half so that his wife and child would get equal portions of the inheritance.

Proposed Budgeting Action Plan

Payoff Outstanding Credit Card Balance

The client has an outstanding credit card balance of $13,000 and only pays the minimum balance every month. The client should pay off his credit card balance in full to avoid the huge 22% interest rate per annum. If not paid in full, the outstanding balance will accumulate every month. This leads to the client paying a higher interest over time. The client should use his savings to pay off the initial $13,000 outstanding credit card balance. The balance for subsequent months would be paid in full.

Payoff Outstanding Credit Card Balance

The client has an outstanding credit card balance of $13,000 and only pays the minimum balance every month. The client should pay off his credit card balance in full to avoid the huge 22% interest rate per annum. If not paid in full, the outstanding balance will accumulate every month. This leads to the client paying a higher interest over time. The client should use his savings to pay off the initial $13,000 outstanding credit card balance. The balance for subsequent months would be paid in full.

Refinancing Car Loan

The client plans to sell his current car and purchase 2 cars, worth $680,000. The Open Market Value (OMV) for the 2 cars are as follows:

Tesla Model Y - $68,691;

Audi e-Tron - $64,068

Since both cars have an OMV of more than $20,000, the client can only take up a 60% loan. The client will need to pay the remaining 40% in cash, which is $272,000. If the client sells his BMW and pays off his outstanding car loan, he will have a total of $190,000 cash. This is not enough to cover the downpayment of the 2 cars. The client will end up using his savings. (refer to Fig 3.3 for breakdown).

Refinancing Car Loan

The client plans to sell his current car and purchase 2 cars, worth $680,000. The Open Market Value (OMV) for the 2 cars are as follows:

Tesla Model Y - $68,691;

Audi e-Tron - $64,068

Since both cars have an OMV of more than $20,000, the client can only take up a 60% loan. The client will need to pay the remaining 40% in cash, which is $272,000. If the client sells his BMW and pays off his outstanding car loan, he will have a total of $190,000 cash. This is not enough to cover the downpayment of the 2 cars. The client will end up using his savings. (refer to Fig 3.3 for breakdown).

Fig 3.3

However, we do not recommend the client to use his savings to purchase the cars as cars will depreciate in value. Furthermore, purchasing more cars is not a necessity. The savings could be better used to invest to fund the client’s retirement and child education which are of higher priority. The client could purchase the 2 cars after he has sufficient funds for his higher priorities.

Fig 3.4

Fig 3.5

Flow Adjustments

The client’s current monthly instalment for car loan is $8,000. The client is recommended to refinance his car loan to increase his cash flow. It is assumed that the client’s current car is approximately 1 year old. In accordance with MAS refinancing rules for motor vehicle loans, the client is able to refinance his car loan to a maximum tenure of 6 years. The client’s outstanding car loan is $120,000. When refinanced with DBS, the new monthly instalment for car loan is $1,945. This is a 75.7% decrease from the current monthly instalment. (refer to Fig 3.4/3.5).

Other Recommendations For Client To Meet Their Budget

When pumping car petrol, the client should source for petrol kiosks which charge a lower price per litre.

Internet service budget can be met through sourcing for service providers offering cheaper plans, can cut down on data usage, or purchase a broadband plan with slower bandwidth.

Health and medical budget can be met through consulting in a polyclinic instead of a private clinic

Dining out budget can be met through cutting down on luxury dinings or cooking at home more often

Alcohol budget can be met through cutting down on liquor as it may harm his health as well

Clothing and personal maintenance budget can be met through purchasing only what is necessary and spending less on luxury products

Public transport budget can be met through purchasing monthly concession card for the child considering that she may take public transport to school daily

Holidays budget can be met through cutting down $2,000 from his usual holiday expenses by finding cheaper accommodations, purchasing a cheaper flight ticket, or cut down on vacation trips

Recreation, TV, Newspapers budget can be met through cutting down on subscription plans for services that the client rarely use

Budget Plan

Other Recommendations For Client To Meet Their Budget

When pumping car petrol, the client should source for petrol kiosks which charge a lower price per litre.

Internet service budget can be met through sourcing for service providers offering cheaper plans, can cut down on data usage, or purchase a broadband plan with slower bandwidth.

Health and medical budget can be met through consulting in a polyclinic instead of a private clinic

Dining out budget can be met through cutting down on luxury dinings or cooking at home more often

Alcohol budget can be met through cutting down on liquor as it may harm his health as well

Clothing and personal maintenance budget can be met through purchasing only what is necessary and spending less on luxury products

Public transport budget can be met through purchasing monthly concession card for the child considering that she may take public transport to school daily

Holidays budget can be met through cutting down $2,000 from his usual holiday expenses by finding cheaper accommodations, purchasing a cheaper flight ticket, or cut down on vacation trips

Recreation, TV, Newspapers budget can be met through cutting down on subscription plans for services that the client rarely use

Budget Plan

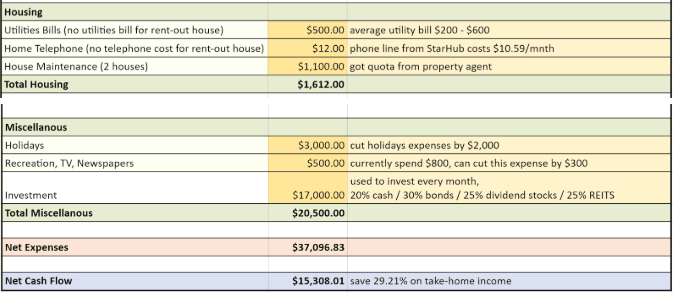

Notes written in the budget plan are for your reference. The estimated net cash flow is $15,308.01. This is 29.21% of the client’s take-home income which will be used for savings. The client will satisfy the general rule of thumb of saving 20% on income. (Refer to Fig 3.6 - Fig 3.8 in the Appendices for relevant details on expenses)

Monitoring and Review of Financial Planning

We will actively monitor market performance and economic indicators to determine if there are any changes that might have an impact on the client’s financial plan. A recession could be brought on due to factors such as high interest rates. The investment strategy will need to be adjusted to reduce risk and protect the client’s assets. Regularly monitoring the market conditions and making adjustments to the plan can help the client achieve their financial goals in a financial environment that is constantly changing.

We will also use economic forecasting tools to efficiently monitor the economy and the market performance. Such tools include trend analysis and econometric models to predict future economic trends and conditions based on historical data and current market trends. Financial market simulation is also another tool that is used to predict economic trends. It uses computer programs to simulate the behaviour of financial markets, which would enable us to comprehend the impacts of various economic scenarios on the client’s financial plan. By incorporating economic forecasting, we will gain valuable insights on the state of the economy as a whole, which would enable us to foresee changes that might impact the financial market. Hence, allowing us to make informed decisions which would be in the best interest of the client.

Additionally, we will schedule frequent check-ins with the client, for example, a bi-annual check-in. Check-ins are to review the client’s financial situation, goals, and any changes in their life that might have an impact on their financial plan. Changes in financial situation would include changes to income, expenses, or debts, and changes in the client’s life can include job loss or a change in the client’s overall health. Their financial objectives and risk tolerance may be impacted by these. Through regular check-ins, we can stay up-to-date on the client’s financial situation and make any necessary changes to the plan. This helps to ensure that the financial plan remains relevant and is aligned to the client’s financial situation and goals.

We will also periodically review statements from the client’s investment accounts. This would entail comparing performance to key benchmarks. Reviewing account statements will help us to assess the performance of the investment portfolio and see if it is on track to achieve the client’s financial goals. Adjustments to the portfolio would be needed if the portfolio is misaligned with the client’s goals. It is also essential to compare the portfolio’s performance to key benchmarks like the S&P 500. This will enable us to assess whether the portfolio is outperforming or underperforming the benchmark and make informed decisions about the portfolio to ensure that the client can reach their financial goals.

We will also regularly review the estate plan. As there may be changes to the client’s will, adjustments to the rules governing estate planning, or adjustments to the client’s own personal situation, like the passing of a spouse, it is important to ensure that the client’s estate plan remains relevant. We can examine these factors and make any required adjustments to the estate plan.

Most importantly, we must communicate to our client frequently about any changes made to their financial plan, and discuss the reasoning behind these changes to ensure that they are on board with the new strategy. This is to ensure that the plan is being followed as per client's requirements.

Additional Appendix

Fig 3.6

Fig 3.7

Notes written in the budget plan are for your reference. The estimated net cash flow is $15,308.01. This is 29.21% of the client’s take-home income which will be used for savings. The client will satisfy the general rule of thumb of saving 20% on income.

(Refer to Fig 3.6 - Fig 3.8 in the Appendices for relevant details on expenses)

Monitoring and Review of Financial Planning

We will actively monitor market performance and economic indicators to determine if there are any changes that might have an impact on the client’s financial plan. A recession could be brought on due to factors such as high interest rates. The investment strategy will need to be adjusted to reduce risk and protect the client’s assets. Regularly monitoring the market conditions and making adjustments to the plan can help the client achieve their financial goals in a financial environment that is constantly changing.

We will also use economic forecasting tools to efficiently monitor the economy and the market performance. Such tools include trend analysis and econometric models to predict future economic trends and conditions based on historical data and current market trends. Financial market simulation is also another tool that is used to predict economic trends. It uses computer programs to simulate the behaviour of financial markets, which would enable us to comprehend the impacts of various economic scenarios on the client’s financial plan. By incorporating economic forecasting, we will gain valuable insights on the state of the economy as a whole, which would enable us to foresee changes that might impact the financial market. Hence, allowing us to make informed decisions which would be in the best interest of the client.

Additionally, we will schedule frequent check-ins with the client, for example, a bi-annual check-in. Check-ins are to review the client’s financial situation, goals, and any changes in their life that might have an impact on their financial plan. Changes in financial situation would include changes to income, expenses, or debts, and changes in the client’s life can include job loss or a change in the client’s overall health. Their financial objectives and risk tolerance may be impacted by these. Through regular check-ins, we can stay up-to-date on the client’s financial situation and make any necessary changes to the plan. This helps to ensure that the financial plan remains relevant and is aligned to the client’s financial situation and goals.

We will also periodically review statements from the client’s investment accounts. This would entail comparing performance to key benchmarks. Reviewing account statements will help us to assess the performance of the investment portfolio and see if it is on track to achieve the client’s financial goals. Adjustments to the portfolio would be needed if the portfolio is misaligned with the client’s goals. It is also essential to compare the portfolio’s performance to key benchmarks like the S&P 500. This will enable us to assess whether the portfolio is outperforming or underperforming the benchmark and make informed decisions about the portfolio to ensure that the client can reach their financial goals.

We will also regularly review the estate plan. As there may be changes to the client’s will, adjustments to the rules governing estate planning, or adjustments to the client’s own personal situation, like the passing of a spouse, it is important to ensure that the client’s estate plan remains relevant. We can examine these factors and make any required adjustments to the estate plan.

Most importantly, we must communicate to our client frequently about any changes made to their financial plan, and discuss the reasoning behind these changes to ensure that they are on board with the new strategy. This is to ensure that the plan is being followed as per client's requirements.

Additional Appendix

Fig 3.6

Fig 3.6

Fig 3.7

Fig 3.7

Fig 3.8

References

Global oil demand set to reach record high as China reopens, IEA says - Financial Times, from https://www.ft.com/content/fb9dde20-96c2-4001-a37d-931fdcac667a

UOB One Savings from https://www.uob.com.sg/onecards/uob-one-account.html

Singapore’s fourth-quarter private housing price growth slows to 0.2 per cent as sales volume falls, (5 Jan 2023) from https://www.scmp.com/business/article/3205638/singapores-fourth-quarter-private-housing-price-growth-slows-02-cent-sales-volume-falls

Global Risks Report 2023, 11 January 2023, from https://www.weforum.org/reports/global-risks-report-2023/

Master Plan, Urban Redevelopment Authority, 3 Feb 2023, from https://www.ura.gov.sg/Corporate/Planning/Master-Plan

Tuition Fees for Graduate (Coursework) Full-Time and Part-Time Programmes for Academic Year 2021-2022 . NTU, from https://www3.ntu.edu.sg/oad2/GA_CW/AY2021-2022CourseworkFees_MOE.pdf

Pruactive_term_ebrochure_english, 8 September 2022, Prudential, from https://www.prudential.com.sg/-/media/project/prudential/pdf/ebrochures/pruactive-term/pruactive_term_ebrochure_english.pdf

Reflection at Keppel Bay PropertyGuru Listing, PropertyGuru, from https://www.propertyguru.com.sg/listing/23827643/for-sale-reflections-at-keppel-bay

Watertown Condo PropertyGuru Listing, PropertyGuru, from https://www.propertyguru.com.sg/listing/24081831/for-sale-watertown

Proposed Budgeting Action Plan

Refinancing Rules for Motor Vehicle Loans. (n.d.). Monetary Authority of Singapore. Retrieved February 4, 2023, from https://www.mas.gov.sg/regulation/explainers/motor-vehicle-loans/refinancing-motor-vehicle-loans

What’s The Cost of Living In Singapore? (2023, January 2). Piloto Asia. Retrieved February 5, 2023, from https://www.pilotoasia.com/guide/cost-of-living-in-singapore

Car Running Costs Singapore 2022. (n.d.). Budget Direct Insurance. Retrieved February 5, 2023, from https://www.budgetdirect.com.sg/car-insurance/research/car-running-costs-singapore

SIM Only Plus mobile plans for business. (n.d.). Singtel Business eShop. Retrieved February 5, 2023, from https://smemobile.bizportal.singtel.com/shops/mobile/new-new-sim-only.jsf

Chan, A. (n.d.). Best Home Fibre Broadband Plan In Singapore 2023. SingSaver. Retrieved February 5, 2023, from https://www.singsaver.com.sg/blog/best-home-fibre-broadband-plan

Digital Voice Home Phone Line. (n.d.). StarHub. Retrieved February 5, 2023, from https://www.starhub.com/personal/home-phone/home-phone-line.html

Vandiver, W., Bradley, S., & Reed, P. (2022, December 8). What Is the Total Cost of Owning a Car? NerdWallet. Retrieved February 5, 2023, from https://www.nerdwallet.com/article/loans/auto-loans/total-cost-owning-car

Lim, A. (2022, January 27). 7 Healthcare Cost Statistics in Singapore (2022): How High Is It? SmartWealth Singapore. Retrieved February 5, 2023, from https://smartwealth.sg/healthcare-cost-statistics-singapore/

Hsu, J. (2021, June 3). How Much Does The Average Singaporean Household Spend Each Month On Groceries? DollarsAndSense.sg. Retrieved February 5, 2023, from https://dollarsandsense.sg/average-singaporean-household-spend-month-groceries/

Cost of Living in Singapore. (n.d.). GuideMeSingapore. Retrieved February 5, 2023, from https://www.guidemesingapore.com/business-guides/immigration/get-to-know-singapore/cost-of-living-in-singapore

Singapore Public Transport: 5 Tips to Save Money on Bus & MRT Fares - MoneySmart.sg. (2021, June 21). MoneySmart blog. Retrieved February 5, 2023, from https://blog.moneysmart.sg/transportation/bus-mrt-fares-public-transport/

Fig 3.8

References

Global oil demand set to reach record high as China reopens, IEA says - Financial Times, from https://www.ft.com/content/fb9dde20-96c2-4001-a37d-931fdcac667a

UOB One Savings from https://www.uob.com.sg/onecards/uob-one-account.html

Singapore’s fourth-quarter private housing price growth slows to 0.2 per cent as sales volume falls, (5 Jan 2023) from https://www.scmp.com/business/article/3205638/singapores-fourth-quarter-private-housing-price-growth-slows-02-cent-sales-volume-falls

Global Risks Report 2023, 11 January 2023, from https://www.weforum.org/reports/global-risks-report-2023/

Master Plan, Urban Redevelopment Authority, 3 Feb 2023, from https://www.ura.gov.sg/Corporate/Planning/Master-Plan

Tuition Fees for Graduate (Coursework) Full-Time and Part-Time Programmes for Academic Year 2021-2022 . NTU, from https://www3.ntu.edu.sg/oad2/GA_CW/AY2021-2022CourseworkFees_MOE.pdf

Pruactive_term_ebrochure_english, 8 September 2022, Prudential, from https://www.prudential.com.sg/-/media/project/prudential/pdf/ebrochures/pruactive-term/pruactive_term_ebrochure_english.pdf

Reflection at Keppel Bay PropertyGuru Listing, PropertyGuru, from https://www.propertyguru.com.sg/listing/23827643/for-sale-reflections-at-keppel-bay

Watertown Condo PropertyGuru Listing, PropertyGuru, from https://www.propertyguru.com.sg/listing/24081831/for-sale-watertown

Proposed Budgeting Action Plan

Refinancing Rules for Motor Vehicle Loans. (n.d.). Monetary Authority of Singapore. Retrieved February 4, 2023, from https://www.mas.gov.sg/regulation/explainers/motor-vehicle-loans/refinancing-motor-vehicle-loans

What’s The Cost of Living In Singapore? (2023, January 2). Piloto Asia. Retrieved February 5, 2023, from https://www.pilotoasia.com/guide/cost-of-living-in-singapore

Car Running Costs Singapore 2022. (n.d.). Budget Direct Insurance. Retrieved February 5, 2023, from https://www.budgetdirect.com.sg/car-insurance/research/car-running-costs-singapore

SIM Only Plus mobile plans for business. (n.d.). Singtel Business eShop. Retrieved February 5, 2023, from https://smemobile.bizportal.singtel.com/shops/mobile/new-new-sim-only.jsf

Chan, A. (n.d.). Best Home Fibre Broadband Plan In Singapore 2023. SingSaver. Retrieved February 5, 2023, from https://www.singsaver.com.sg/blog/best-home-fibre-broadband-plan

Digital Voice Home Phone Line. (n.d.). StarHub. Retrieved February 5, 2023, from https://www.starhub.com/personal/home-phone/home-phone-line.html

Vandiver, W., Bradley, S., & Reed, P. (2022, December 8). What Is the Total Cost of Owning a Car? NerdWallet. Retrieved February 5, 2023, from https://www.nerdwallet.com/article/loans/auto-loans/total-cost-owning-car

Lim, A. (2022, January 27). 7 Healthcare Cost Statistics in Singapore (2022): How High Is It? SmartWealth Singapore. Retrieved February 5, 2023, from https://smartwealth.sg/healthcare-cost-statistics-singapore/

Hsu, J. (2021, June 3). How Much Does The Average Singaporean Household Spend Each Month On Groceries? DollarsAndSense.sg. Retrieved February 5, 2023, from https://dollarsandsense.sg/average-singaporean-household-spend-month-groceries/

Cost of Living in Singapore. (n.d.). GuideMeSingapore. Retrieved February 5, 2023, from https://www.guidemesingapore.com/business-guides/immigration/get-to-know-singapore/cost-of-living-in-singapore

Singapore Public Transport: 5 Tips to Save Money on Bus & MRT Fares - MoneySmart.sg. (2021, June 21). MoneySmart blog. Retrieved February 5, 2023, from https://blog.moneysmart.sg/transportation/bus-mrt-fares-public-transport/